Welcome to TRUSTLINK

Tax Benefits Guide for Salaried Employees: tax planning as a salaried professional means balancing monthly take-home pay with long-term wealth building. For Assessment Year (AY) 2026-27, the Income-tax Act, 1961 (as amended by the Finance Act, 2026) offers significant relief through expanded standard deductions, higher rebate thresholds under the concessional tax regime, and a simplified compliance framework.

Whether you are opting for the streamlined New Tax Regime or maximizing itemized deductions under the Old Tax Regime, structuring your pay and investments correctly can substantially lower your tax liability. Here is your complete reference guide to salaried tax benefits, organized cleanly using a parallel structure to business guides.

Table of Contents

A. Simplified Tax Regimes (New vs. Old Regime Computation)

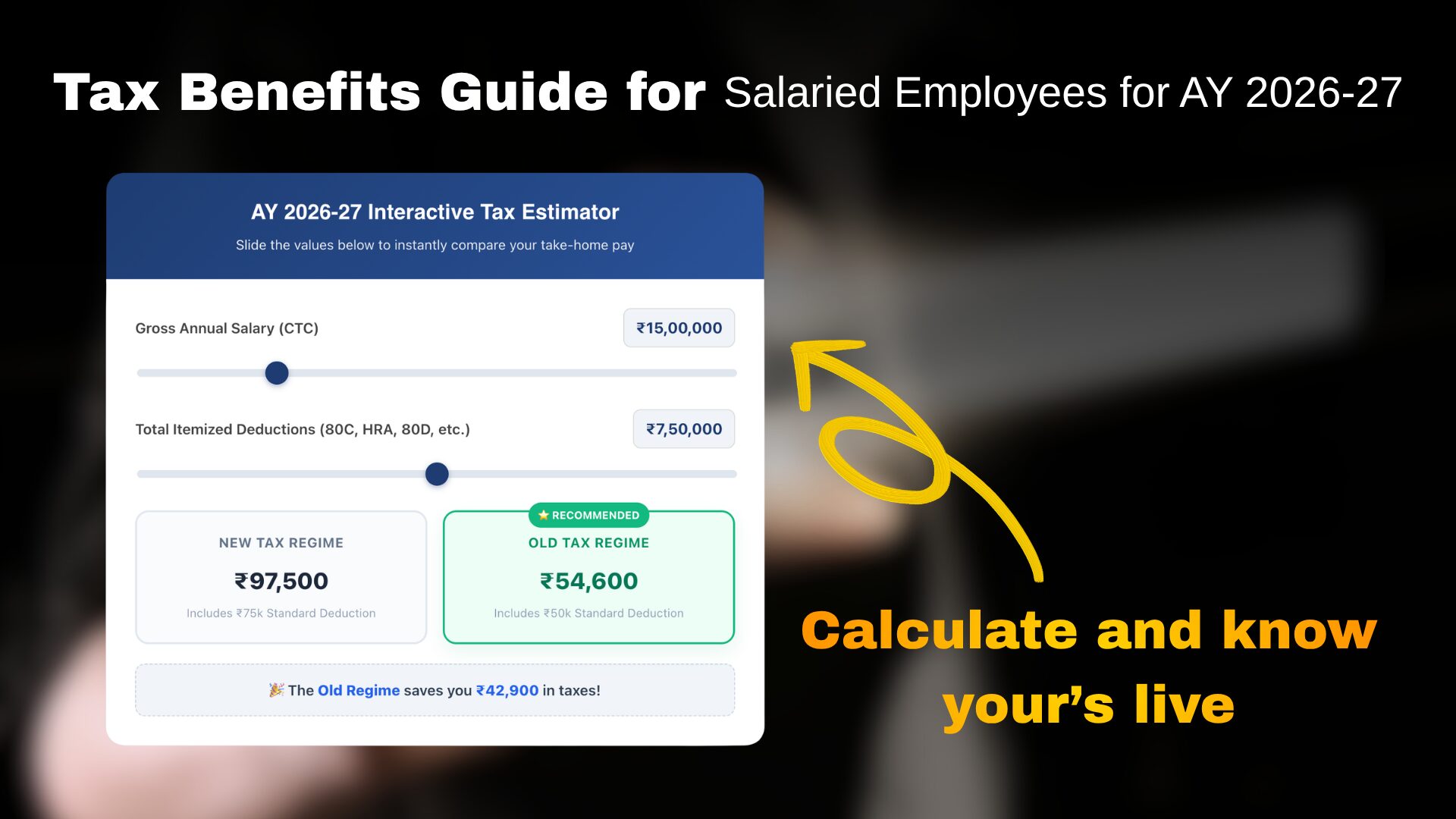

Under Section 115BAC, salaried employees can choose between two distinct methods of income computation each financial year. The New Tax Regime serves as the default option, designed to eliminate paperwork by replacing dozens of complex exemptions with lower upfront tax rates.

| Feature / Metric | New Concessional Tax Regime (Section 115BAC) | Old Tax Regime (Standard Provisions) |

| Default Status | Yes (Default regime for AY 2026-27). Must explicitly opt out to use the old rules. | No (Optional regime). Chosen by employees with heavy itemized deductions. |

| Basic Exemption Limit | Rs. 4,00,000 (No tax payable up to this basic slab). | Rs. 2,50,000 (Rs. 3 lakh for Senior Citizens; Rs. 5 lakh for Super Senior Citizens). |

| Standard Deduction | Rs. 75,000 flat deduction from gross salary. | Rs. 50,000 flat deduction from gross salary. |

| Major Exemptions Allowed | Very limited (Standard Deduction, employer NPS contribution under Section 80CCD(2)). | Comprehensive (HRA, LTA, Section 80C, 80D medical, home loan interest, etc.). |

| Flexibility for Salaried | Can switch back and forth between regimes every financial year. | Can switch back and forth every financial year (unless you also have business income). |

AY 2026-27 Interactive Tax Estimator

Slide the values below to instantly compare your take-home pay

⭐ RECOMMENDED

New Tax Regime

₹ 0

Includes ₹75k Standard Deduction

⭐ RECOMMENDED

Old Tax Regime

₹ 0

Includes ₹50k Standard Deduction

B. Direct Salary Deductions & Allowances (Standard Deduction, HRA, LTA)

If you opt for the Old Tax Regime, structuring your monthly salary components effectively allows you to claim direct operational deductions against your compensation.

| Section / Allowance | Category | Deduction & Exemption Rule |

| Section 16(ia) | Standard Deduction | Flat deduction of Rs. 75,000 under the New Regime and Rs. 50,000 under the Old Regime, requiring no receipt proofs. |

| Section 16(ii) & (iii) | Entertainment & Professional Tax | Professional tax paid is fully deductible (Old Regime). Entertainment allowance is deductible only for government employees (up to Rs. 5,000). |

| Section 10(13A) | House Rent Allowance (HRA) | Exempt under Old Regime to the least of: actual HRA received, 50% of basic salary (for metro cities) or 40% (non-metro), or actual rent paid minus 10% of basic salary. |

| Section 10(5) | Leave Travel Allowance (LTA) | Exemption on travel expenses for the employee and family for two domestic journeys in a block of four calendar years (Old Regime only). |

| Section 10(14) | Special Allowances | Daily allowance, uniform allowance, and academic research allowance are exempt to the extent actually incurred for professional duties (Old Regime). |

C. Documentation, Compliance & ITR Filing Reliefs

Salaried individuals benefit from a significantly streamlined compliance burden compared to business owners, with automated reporting and reduced paperwork.

- Exemption from Accounting & Audits (Section 44AA / 44AB): Salaried employees have zero obligation to maintain formal books of account or undergo statutory tax audits, regardless of how high their compensation package scales.

- Single-Form Compliance (Form 16): Your employer consolidates your annual earnings, tax deductions, and exemption proofs into a standardized Form 16 (Parts A & B), serving as the primary document required for filing.

- Pre-Filled Returns (AIS / TIS): The Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) automatically populate salary income, bank interest, dividend payouts, and tax deducted, reducing manual entry errors during ITR-1 or ITR-2 filing.

D. Chapter VI-A Deductions & Wealth-Building Incentives

For employees sticking with the Old Tax Regime, Chapter VI-A provides robust avenues to reduce taxable income while building long-term retirement and healthcare safety nets.

| Section | Investment / Expense Type | Maximum Deduction Limit |

| Section 80C | PF, PPF, ELSS Funds, Life Insurance Premiums, Home Loan Principal | Aggregate deduction up to Rs. 1,50,000 per financial year. |

| Section 80CCD(1B) | National Pension System (NPS) – Employee Contribution | Additional deduction up to Rs. 50,000 over and above the Section 80C limit. |

| Section 80CCD(2) | NPS – Employer Contribution | Deduction up to 14% of salary (Basic + DA) for government employees and 10% for private sector employees (Available in BOTH New and Old Regimes). |

| Section 80D | Health Insurance Premiums & Preventative Checkups | Up to Rs. 25,000 for self/family (Rs. 50,000 if senior citizen), plus up to Rs. 50,000 for parents’ insurance (Rs. 50,000 if senior citizens). |

| Section 24(b) | Home Loan Interest (Self-Occupied Property) | Deduction up to Rs. 2,00,000 per year on interest paid toward buying or constructing a self-occupied home (Old Regime only). |

| Section 80E | Education Loan Interest | 100% of interest paid on higher education loans for self, spouse, or children, claimable for up to 8 consecutive years. |

| Section 80G | Charitable Donations | 50% or 100% deduction on contributions made to recognized charitable funds and relief trusts (Old Regime only). |

E. TDS on Salary (Section 192) & Advance Tax Rules

Salaried professionals enjoy automated tax compliance, with employers handling the bulk of tax calculations and deposits directly to the government.

- Tax Deduction at Source (Section 192): Employers are legally required to estimate an employee’s annual income, apply the relevant tax slabs, and deduct TDS proportionately across 12 monthly paychecks.

- Declaring Other Income: You can declare external income (such as savings account interest, capital gains, or rental income) to your employer. They will adjust your monthly TDS accordingly, preventing a lump-sum tax burden at year-end.

- Exemption from Advance Tax (Section 207 / 208): If your entire tax liability is covered via TDS under Section 192 and your remaining net tax payable is less than Rs. 10,000, you are completely exempt from paying quarterly advance tax installments. Senior citizen salaried employees with no business income are also entirely exempt from advance tax.

F. Basic Exemption Limits & Tax Rebates (AY 2026-27)

The Finance Act, 2026 establishes clear exemption thresholds and tax rebates designed to insulate middle-income salaried earners from tax liability.

| Tax Regime / Category | Basic Exemption Slab (Zero Tax) | Section 87A Rebate Income Threshold | Maximum Rebate Amount |

| New Concessional Regime (Section 115BAC) | Rs. 4,00,000 (Standard across all age brackets). | Total taxable income up to Rs. 12,00,000 | Up to Rs. 60,000 (Makes net tax payable Nil for taxable income up to Rs. 12 lakh). |

| Old Tax Regime (Standard Salaried Under 60) | Rs. 2,50,000 | Total taxable income up to Rs. 5,00,000 | Up to Rs. 12,500 |

| Old Tax Regime (Senior Citizens aged 60 to 79) | Rs. 3,00,000 | Total taxable income up to Rs. 5,00,000 | Up to Rs. 12,500 |

| Old Tax Regime (Super Senior Citizens aged 80+) | Rs. 5,00,000 | Not Applicable | Basic exemption covers up to Rs. 5 lakh. |

G. Special Tax Reliefs & Retirement Benefits (Gratuity, PF, Leave Encashment)

When transitioning jobs or reaching retirement, salaried employees receive statutory payouts that benefit from dedicated tax exemptions under Section 10.

- Gratuity (Section 10(10)): Fully tax-exempt for government employees. For private sector employees covered under the Payment of Gratuity Act, exemption is allowed up to Rs. 20 lakh (calculated as 15 days of last drawn salary for every completed year of service).

- Leave Encashment (Section 10(10AA)): Cash received for unused earned leave at retirement is completely tax-free for government staff. For private employees, the statutory tax exemption limit stands at Rs. 25 lakh.

- Employee Provident Fund (EPF): Lump-sum withdrawals from a recognized provident fund are 100% tax-exempt, provided the employee has completed 5 continuous years of service.

- Retrenchment & Voluntary Retirement (VRS): Compensation received on retrenchment is exempt up to Rs. 5 lakh, while payouts received under approved Voluntary Retirement Schemes (Section 10(10C)) are tax-free up to Rs. 5 lakh.

H. Simplified Return Filing & Exemption from e-Filing

The tax administration simplifies the return filing process for salaried individuals through tailored forms and senior citizen exemptions.

- ITR-1 (Sahaj): The simplest return form, available to resident individuals having total income up to Rs. 50 lakh consisting of salary, one house property, and other sources (interest/dividends).

- ITR-2: Required if you are a salaried employee with capital gains from stock trading/mutual funds, foreign assets, or more than one house property.

- Exemption for Super Senior Citizens (Section 194P): Salaried individuals or pensioners aged 75 years and above are completely exempt from filing an income tax return if their only income consists of pension and bank interest received in the same specified bank, provided the bank deducts the exact tax due at source.